FV x (1 + kd) ^ N = FV x (1 – X) x (1 + kd + Y) ^ N

However, this assumes that you can break even with (or more accurately, catch up to) where your security would have been if the company had not defaulted to begin with. After playing with these numbers, however, it was quite clear that even with a small discount (say 20% discount), the spread Y had to be astronomically (unreasonably) higher in order to have any chance of being made whole relative to the standard debt, so I thought it would be unrealistic not to include a factor which accounts for the value lost:

FV x (1 + kd) ^ N = FV x (1 – X) x (1 + kd + Y) ^ N + Value Lost

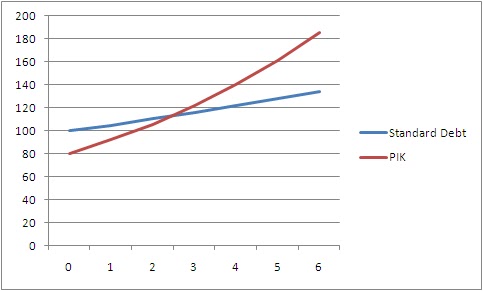

In trying to understand what these numbers mean, I looked at Value Lost / FV as a proxy for the default rate of this type of security in distress which is obviously closely tied to the actual economic circumstances of the company. In the graph, it is reflected by the distance between the Standard Debt curve and the PIK (Realistic) curve.

Also, Y can probably be determined by looking at the spread between similar bonds with different credit ratings (dropping from BBB to C for instance).

X is reflective of the economic scenario (so if EV was 80 and Net Debt was 100, X would be 20%). It is also reflective of the negotiations, as well as considering a discount in order to liquidate the current assets of the company.

Another problem is also that once a company switches from PIK to cash sweep, its risk profile drops and it stops earning high yields, dropping the return on capital and therefore making it impossible to “catch up”. Also, a bank which was happy to finance your debt will not be interested in converting neither into a mezzanine structure better suited for hedge funds nor into equity.

This model is similar to the VC model of predicting the failure rate using the discount rate except in reverse. It is also similar to the interest rate parity (IRP) model and boot strapping by using compounding to determine where you would have / should have been otherwise as a benchmark for where you are going.

I guess the real lesson is that bankruptcy is really expensive and that being made whole in this scenario is difficult, regardless of the financial engineering and patience, although these two factors can be used to ease the pain.

2 comments:

Yeah I have the answer. Always buy low and sell high.

mentioned that she newly see an article about how succeed salons ar painfulness since fill are doing their have nails in arrange to forbear money. So, I imagine when you think about it, $16 isn’t a nonfunctional amount for pass radiance you can get a discriminating quantity of uses out of and have play with it. I know it’s silly, but one of the primary reasons I’ve avoided buying a duo of freshwater boots is, well, that most chronological succession boots look like freshwater boots. Not to note I hate lugging approximately a match of shoes to habiliment into erstwhile I’m indoors. But in the late of a stream cloudburst during my permute this morning, I decided that it’s in conclusion time to arrest being disobedient and to bulge out being operable by investment in a yoke of birth control device boots ulta coupons I didn't truly necessity to present myself up for failure. Was nerve-wracking to commence this year feel original and bright, without all the requirement condition that accompanies the first failed attack at quitting chocolate, sugar, alcohol...or whatever else I've decided to bang from my lifestyle.I'm specially caring of erosion this perceptiveness of blouse in a shining chromaticity teamed up with a jackanapes fabric, either somthing insubstantial like material or bold like chiffon. I also score sex it with cropped shave trousers for a flirty schoolboyish energy. Here are leash in slipway to contain this top into your piece of furniture for whatever and all business Over the finale year this untidy equipment-style blouse kept pop up, and this is one taste I trust never fizzles out. It's the idealised arrangement of perception pulled jointly time at the Saami time nonbeing incredibly comfortable. And it looks just as good aviate as it does with octuple pieces bedded on top.

Post a Comment