FV x (1 + kd) ^ N = FV x (1 – X) x (1 + kd + Y) ^ N

However, this assumes that you can break even with (or more accurately, catch up to) where your security would have been if the company had not defaulted to begin with. After playing with these numbers, however, it was quite clear that even with a small discount (say 20% discount), the spread Y had to be astronomically (unreasonably) higher in order to have any chance of being made whole relative to the standard debt, so I thought it would be unrealistic not to include a factor which accounts for the value lost:

FV x (1 + kd) ^ N = FV x (1 – X) x (1 + kd + Y) ^ N + Value Lost

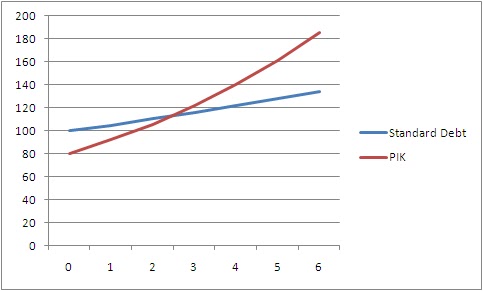

In trying to understand what these numbers mean, I looked at Value Lost / FV as a proxy for the default rate of this type of security in distress which is obviously closely tied to the actual economic circumstances of the company. In the graph, it is reflected by the distance between the Standard Debt curve and the PIK (Realistic) curve.

Also, Y can probably be determined by looking at the spread between similar bonds with different credit ratings (dropping from BBB to C for instance).

X is reflective of the economic scenario (so if EV was 80 and Net Debt was 100, X would be 20%). It is also reflective of the negotiations, as well as considering a discount in order to liquidate the current assets of the company.

Another problem is also that once a company switches from PIK to cash sweep, its risk profile drops and it stops earning high yields, dropping the return on capital and therefore making it impossible to “catch up”. Also, a bank which was happy to finance your debt will not be interested in converting neither into a mezzanine structure better suited for hedge funds nor into equity.

This model is similar to the VC model of predicting the failure rate using the discount rate except in reverse. It is also similar to the interest rate parity (IRP) model and boot strapping by using compounding to determine where you would have / should have been otherwise as a benchmark for where you are going.

I guess the real lesson is that bankruptcy is really expensive and that being made whole in this scenario is difficult, regardless of the financial engineering and patience, although these two factors can be used to ease the pain.

Discounted Cash Flow Model

Discounted Cash Flow Model

Dave is interested in buying Steve's house. For simplicity, let's say the house hasn't appreciated in value and is still worth $100k. Dave doesn't care what Steve's mortgage is, how much he's paid down etc. After all, that is Steve's capital structure. Dave is a new home buyer and is starting with a $20k downpayment and $80k mortgage.

Dave is interested in buying Steve's house. For simplicity, let's say the house hasn't appreciated in value and is still worth $100k. Dave doesn't care what Steve's mortgage is, how much he's paid down etc. After all, that is Steve's capital structure. Dave is a new home buyer and is starting with a $20k downpayment and $80k mortgage.  The main point is that it doesn't matter who is buying the house (over simplified assumption), the house is worth $100k. It is an attempt to understand an unbiased (unlevered) way of looking at value of the company.

The main point is that it doesn't matter who is buying the house (over simplified assumption), the house is worth $100k. It is an attempt to understand an unbiased (unlevered) way of looking at value of the company.

Well it would be the same as the PV's value at time n, discounted back to 0. Since the cash flows at time n would look the same as now, the PV at time n should be the same as the PV now.

Well it would be the same as the PV's value at time n, discounted back to 0. Since the cash flows at time n would look the same as now, the PV at time n should be the same as the PV now. (Note this graph is merely the first graph minus the second graph in the same way the math is the first PV minus the second.)

(Note this graph is merely the first graph minus the second graph in the same way the math is the first PV minus the second.)